Gamuda climbs to new peak, driven by A$1.6b job win in Australia and optimism in construction sector

- by Admin

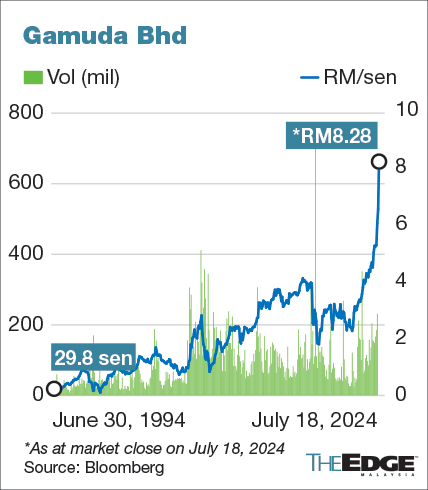

- July 18, 2024

KUALA LUMPUR (July 18): Shares in Gamuda Bhd (KL:GAMUDA) surged to a new record high on Thursday, boosted by news that its joint venture (JV) in Australia secured a contract worth A$1.6 billion (RM5 billion) and renewed interest in construction stocks on Bursa Malaysia.

Gamuda increased as much as 2.91% to reach an intraday high of RM8.49 after the midday trading break. The stock pared some of its gains and closed 0.36% or three sen higher at RM8.28, still its highest closing price since the group was first listed in 1992, valuing the construction giant at RM22.96 billion.

Gamuda’s share price has soared 42% over the past two months.

At its current market capitalisation, Gamuda is already the 21st largest company on Bursa Malaysia, making it poised to be a potential FBM KLCI constituent. The next review of the benchmark index will be on Dec 24 and it is already under the FBM KLCI Reserve List.

Construction stocks have broadly outperformed other sectors this year, largely fuelled by optimism about the government’s roll-out of major infrastructure projects. A slew of highly lucrative jobs, particularly to build data centres, has also boosted shares of select companies, including Gamuda.

The Bursa Malaysia Construction Index, which tracks 49 stocks in the sector, rose 0.36% to close at 316.83 points on Thursday, its highest since February 2018. Year to date, the index has gained over 65%.

Analysts bullish on Gamuda

A majority of analysts tracking the construction group are bullish on its prospects. Of the 20 research houses covering Gamuda, 17 have “buy” calls, while two have a “hold” rating. Only one — BIMB Securities Sdn Bhd — has a “sell” rating. According to Bloomberg, the consensus 12-month target price is RM7.73, which Gamuda has surpassed.

“You are right in pointing out that Gamuda’s current price has surpassed most of the street’s target prices, including ours at RM7.50. We are in the midst of reviewing our target price,” MIDF Research construction analyst Royce Tan told The Edge.

With construction being among the hottest sectors in Malaysia right now, Tan said that it is no surprise that Gamuda remains on top of the pecking order with its bulging order book of RM26.5 billion, which he added, “will only grow bigger from this point.”

“The Penang LRT contract itself will push the outstanding orderbook beyond RM30 billion once it is formalised, on top of the other civil projects where it is a frontrunner. Based on our observations, we note that the recent rally was very much driven by foreign institutional investors who have net bought RM331.4 million of Gamuda shares month-to-date,” he said.

On top of its current bulging orderbook, Gamuda on Thursday said its JV with French rail engineer Alstom SA in Australia has secured a contract worth A$1.6 billion to upgrade and automate signalling and train control systems in Perth’s suburban rail networks.

Gamuda has a 46% stake in the JV, while Alstom holds the remaining 54%. As such, Gamuda is expected to rake in revenue of up to A$737 million (approximately RM2.3 billion) from its involvement in the project, the contract of which will last over 10 years.

RHB Investment Bank equity research analyst Adam Mohamed Rahim, who has a higher-than-consensus target price of RM9.68 for Gamuda, said the latest announcement is within the bank’s expectations as the Western Australian government had announced in April that Gamuda’s JV with Alstom was selected as the preferred proponent for the said high-capacity signalling job in Perth.

“We believe the share price rally still has legs, especially if Gamuda manages to clinch new data centre (DC) jobs going forward,” he told The Edge.

Adam said the slew of announcements on new DC investments has boosted business sentiment and uplifted interest in Gamuda, given that it secured its first DC job from Sime Darby Property Bhd (KL:SIMEPROP) and Pearl Computing Malaysia. Other analysts concur, foreseeing that Gamuda is poised to bag more project portfolios in the DC sector.

“We also note that its IBS (Industrialised Building System) factories in Banting and Sepang can accommodate around two to three DC jobs with a cumulative capacity of up to around 200MW concurrently, in our view,” he added.

Bucking the trend, however, an analyst who requested not to be named contended that Gamuda’s valuations are “totally irrational”, saying that market sentiment is overly bullish.

The analyst pointed out that the recent job win is to be implemented over the course of 10 years, which is longer than Gamuda’s other typical jobs which last only up to four years.

“So I would say if anything, actually this kind of win would be negative for short-term earnings forecasts, because they basically have to spread out their orderbook consumption.

“The problem with these Australian jobs is that the margins are about half of what they are in Malaysia. So the challenge for Gamuda is that while the orderbook sum looks big, the margin might be much less. So they almost have to run twice as hard to get to the same spot,” the analyst added.

The Latest News

-

December 23, 2024TaylorMade drops Hall-of-Fame Christmas posters starring Tiger Woods, Rory McIlroy and Nelly Korda – Australian Golf Digest

-

December 23, 2024Here’s why Golf Twitter lost its damn mind over Team Langer’s PNC victory – Australian Golf Digest

-

December 23, 2024Social Media Ban in Australia: What Online Casinos Can Learn on Responsible Gambling Practices? – Insights from CasinoAus

-

December 23, 2024From smaller homes to screen time, backyard cricket is facing challenges in modern Australia

-

December 23, 2024This quiet Canadian will make you love YouTube golf again – Australian Golf Digest

{kind=link}