Higher living costs are eating into your super. Here’s what to do

- by Admin

- May 17, 2024

But the erosive effects of inflation on retirees’ purchasing power is significant, says Integro Private Wealth director Tim Sullivan. “Cash and term deposits typically offer fixed interest rates that may not always keep pace with inflation. As the cost of living rises, the real value of these assets diminishes over time. Inflation also affects retirees differently, as their spending patterns may be concentrated in areas experiencing higher price increases, such as everyday goods and services.”

Many retirees dial down their exposure to riskier growth assets too early, adds Billy Amiridis, of 360 Financial Strategists. This tendency has been exacerbated as rates have increased, tempting retirees to move more money into term deposits.

“It’s very easy for somebody who knows and loves term deposits to say, ‘OK great, a term deposit is paying 4.5 per cent, let’s just move back to that’, because they know it, they understand it and in their mind it [lessens] risk,” Amiridis says.

But there is also a risk that whatever money you make on a term deposit will be eliminated by the commensurate increase in living costs.

“Look at investments that are inflation linked,” Amiridis says. “Make sure the business or the industry you invest in has the option to pass on increases without too much resistance – things like infrastructure, energy and transport.”

Real estate investment trusts are another option, he says. “A commercial property REIT will involve a tenant who has a CPI increase each and every year. Having the right type of asset is important, though, and that’s probably not office towers or discretionary retail at the moment,” he says.

One way to insulate an investment portfolio from inflation is by owning high-quality infrastructure assets, says financial adviser Rob Pizzichetta. Eamon Gallagher

Infrastructure

Another way to insulate an investment portfolio from inflation is by owning high-quality infrastructure assets.

“Infrastructure assets with earnings contracted and regulated to rise at or greater than the rate of inflation work in high inflationary periods,” says Rob Pizzichetta, a financial adviser and founder of Mont Wealth.

“These assets have never looked this attractive given the decarbonisation theme, transition to renewables, and growing usage of artificial intelligence.”

Lazard Asset Management’s Robertson says it makes sense to own shares in businesses that own ports, toll roads, airports, or other high-quality infrastructure for two principal reasons.

First, the assets and profits should rise in value at least in line with inflation. This means dividends should rise too, as what the businesses charge customers is often indexed – that is, prices rise with inflation.

Second, the potential for an inflation-induced downturn bolsters the case for infrastructure assets because their revenue and profit streams are defensive versus businesses linked to discretionary spending or economic growth such as the banks. In short, ports and toll roads will continue to charge customers even in a recession.

“Traffic patterns on roads and airports don’t see the same impact as people cutting spending at their local Italian restaurant or on male underpants,” Robertson says.

But not all infrastructure is created equal, Robertson adds. “Of about 400 listed stocks around the world about 100 hit the sweet spot of being an essential service, monopolistic, and having inflation-protected attributes,” he says.

On the ASX, Robertson likes dominant $26.7 billion market cap toll road operator Transurban and rival toll roads merchant Atlas Arteria.

Transurban offers a yield of 4.8 per cent for investors, based on trailing dividends of 61.5¢ per share over the past 12 months, with Atlas Arteria paying a 7.3 per cent yield based on trailing dividends of 40¢ per share and a $5.47 stock price.

Superannuation funds are heavy investors in infrastructure (more on that later) but a retail investor seeking exposure to infrastructure outside super could use an exchange-traded fund.

A wholesale investor, such as the trustee of a self-managed super fund, could use a fund that owns unlisted infrastructure assets.

Private credit

Pizzichetta says another option is to consider buying into private credit funds, some of which offer inflation-beating yields above 8 per cent.

Loans made by the funds to corporate borrowers are often priced at a fixed margin above benchmark interest rates, which means they give some insurance against central banks keeping rates high to tame inflation.

But beware the charlatans.

“With higher risk, a higher reward is required,” Pizzichetta says. “It’s important to find a private credit fund manager that has a strong track record of performance, strong relationship with its borrowers, and an ability to manage a default if required.

“At present, private credit funds yield 8 to 10 per cent without having to take too much risk, providing investors an inflation-proof retirement plan. We recommend a higher allocation to private credit funds for income and growth-seeking investors.”

Cash

To protect against a downturn, the king of defensive assets – cash – is another option. It’s free of risk, and highly likely to outperform falling stocks and other risk assets in a recession, according to Robertson.

However, as mentioned above, if you hold too much you’re vulnerable to the impact of inflation, as one dollar today will only be worth around 96¢ this time next year if inflation reaches 4 per cent, says Andrew Darroch, the founder of Independent Wealth Advice.

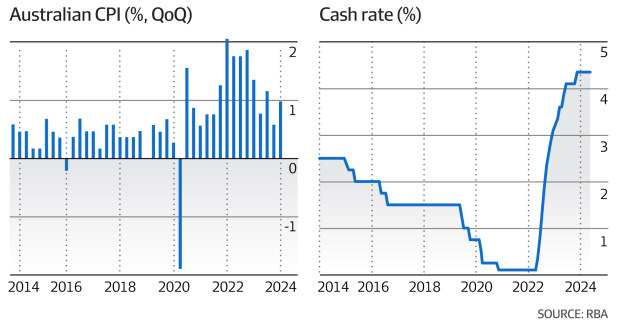

Many banks offer savings rates of more than 5 per cent on an introductory basis, but over the medium term it’s tough to obtain more than the RBA’s 3.8 per cent forecast for inflation, according to financial comparison site Finder.

Darroch says younger investors can afford to risk more through a cycle and hold far less cash as a percentage of investment assets, versus retirees.

“Do I want to go to cash and miss out on an equities rally should there be a surprise drop in inflation and a commensurate lowering of rates? Absolutely not,” says Darroch.

Darroch also dismisses the idea that owning blue-chip miners such as BHP, Newmont or Rio Tinto can help you hedge against inflation, as commodity prices tend to rise as the value of money is eroded. “We’ve got a geopolitical mess, protectionist trade and enormous uncertainty around China,” he says.

The professional planner says the rules for investing in the current climate should really be little different from the pre-pandemic period of low inflation. The strategy for any investor is more a function of personal circumstances, than trying to predict an uncertain future, he says.

“The debate over inflation and interest rates is a discussion that changes daily. One minute the market’s calling rates to fall, the next to rise. So fiddling about with strategies or your portfolio too much, doesn’t make sense.”

Industry super funds

Darroch argues industry super funds offer the best risk-adjusted returns because they have the scale and financial firepower to own the world’s best assets.

“Industry funds represent one the few investments in Australia, irrespective of a person’s investable wealth, to provide truly robust asset allocation,” he says.

“They’re unrivalled in cost, quality and liquidity, specifically, an ability to forgo it. They’ve the scale to gain better quality, and better diversification, for example they can buy a property portfolio of hospitality and healthcare investments with inflation-linked leases. Or a portfolio of infrastructure investments will often incorporate inflation-linked increases.

“Do I want to be locked up in a third-grade retail property fund, private equity fund, or private credit fund? Absolutely not.”

Annuities

Other professional investors tout inflation-linked annuities as an alternative way to protect a retiree’s buying power from inflation. Some pay monthly income in line with inflation, and there is an argument that this helps retirees maintain a worry-free lifestyle.

Using a portion of a portfolio to purchase a CPI-protected annuity can provide a respite if higher inflation lingers. But Darroch does not like them as an investment. “Annuities don’t offer a compelling enough return, full stop,” he says.

“The return is much less desirable when you consider the lifetime commitment, counterparty risk, removal of estate and ability to bequeath. They do offer limited Centrelink benefits, but are only really appropriate for an investor with no capacity to tolerate market fluctuations.”

But Aaron Minney, the head of retirement income at Challenger, which sells inflation-linked annuities, says many retirees don’t have time to ride out the effects of inflation on their portfolios.

His research suggests that obtaining real returns – that is above inflation – in equities over the past 100 years has required a 16-year investment horizon. A 70/30 fund (70 per cent growth assets such as equities and 30 per cent defensive) needed 20 years and a 50/50 fund 25 years.

Spend less, work longer

This probably isn’t a very palatable option for many retirees or would-be retirees and Amiridis urges his clients to think about it like this: “You can work another five years and spend less but your quality of life declines.

“What we try to look at is the shape of the retirement income. It makes sense to spend more money in the early years of retirement when you’ve got the time and the energy to tick off all the costlier, big-ticket items on your bucket list. Make the sacrifices towards the end once you’ve seen the sights and done all those things. There is also a government safety net in the form of the age pension.”

A bucket strategy

Aaron Kane from EK Financial Group says “bucketing” helps shield his clients from inflation.

Let’s say you have $1 million in super and want to draw 5 per cent which is $50,000.

Into the first bucket goes one year’s income in cash, which is used to pay a fortnightly or monthly super pension.

Bucket two is “filled” with a term deposit with a term of one year and $50,000.

“At the moment, you’re getting just over 5 per cent on that term deposit. So there we have two buckets with two years of income guaranteed risk-free.”

In bucket three is another term deposit but of a longer duration.

“Maybe that’s a two-year term, so we’re getting high 4 per cents on it. To that we might add some higher-yield, lower-risk assets like mortgage-backed securities or managed funds paying a decent monthly income of between 5 per cent and 8 per cent to the client.”

Bucket four is home to growth assets such as domestic and international shares.

“Because we’ve created our own defensive position with cash and term deposits, it allows a client to go higher growth in that last bucket without compromising on, say, a 50:50 overall growth defensive split,” Kane says.

“That fourth bucket is going to be volatile, but it will pay dividends to top up cash bucket one. If the market is up at our annual review we might also top up the defensive buckets. If the market is down, we don’t touch bucket four.”

Integro Private Wealth’s Sullivan also likes to take a bucketing approach.

“Regular rebalancing and periodic adjustments to each bucket’s asset allocation ensures that the portfolio remains aligned with evolving financial needs and market conditions,” he says.

“Overall, the investment bucket approach provides retirees with a structured framework for managing risk and optimising returns throughout their retirement years.”

The Latest News

-

December 23, 2024Kyrgios return ‘super exciting’ for Australian tennis says Alex de Minaur

-

December 23, 2024‘Got some good bants’: Hilarious stump mic warning as Konstas plots secret Bumrah counter

-

December 23, 2024Former AFL player Aaron Shattock fighting for life after excavator accident

-

December 23, 2024Naomi Osaka questions Nike in statement regarding Australian Open outfits

-

December 23, 2024Aussie NFL Wrap-up: How did Jordan Mailata, Tory Taylor, and more perform in Week 16? | Sporting News Australia